Everyone’s favourite time of year is coming up! Tax season can be a stressful time for a lot of Canadians, but although they might seem complicated, Canadian taxes can actually be quite simple. Read on to learn the basics and find out what you need to know.

This post may contain affiliate links, which means I may receive a commission, at no extra cost to you, if you make a purchase through a link. As an Amazon Associate, I earn from qualifying purchases. Please see my full disclosure for further information.

There is a very common statement about how there are two sure things in life: Death & Taxes. It is an unfortunate necessity in life in Canada. However, like everything to do that involves money, it is just one part of the game.

So, learn the game and play it appropriately but legally. Speaking with a tax expert to avoid problems and pay less tax is always in your best interest.

So, how do we play the game? Start with who is supposed to file taxes. In short, everyone who earns money, regardless of age.

However, if you are under the age of majority in your home province and did not earn any income, you are most likely not required to file your taxes for that year.

So, all adult Canadian residents and some minors need to file taxes every calendar year, but what about couples, can they file jointly? It is pretty simple in Canada: everyone files a separate income tax declaration. However, married or common-law partners have their incomes calculated as a family unit.

I have seen with some couples that they really don’t want their significant other to know anything about their finances.

That is their choice, but this is an issue because the governments need to understand how to assess the family unit.

So, at the very minimum, you or your tax preparer must include your significant other’s basic information, such as their name, Social Insurance Number, Date of birth, and their worldwide net income.

Yes, worldwide income, because citizens of Canada need to declare ALL the money they made around the world. There are some exceptions to this, so ask your professional tax advisor.

Software or tax return booklet?

This question is far less frequent now, as few people remember getting the tax booklet from the Canada Revenue Agency or Revenu Québec.

As a professional tax preparer, I highly recommend using tax software to prepare your taxes. Most software is user-friendly and only asks for relevant information about your situation.

It also allows for possibilities that you may not have thought of. When preparing for family units, many software also look for the best possible money-saving outcome.

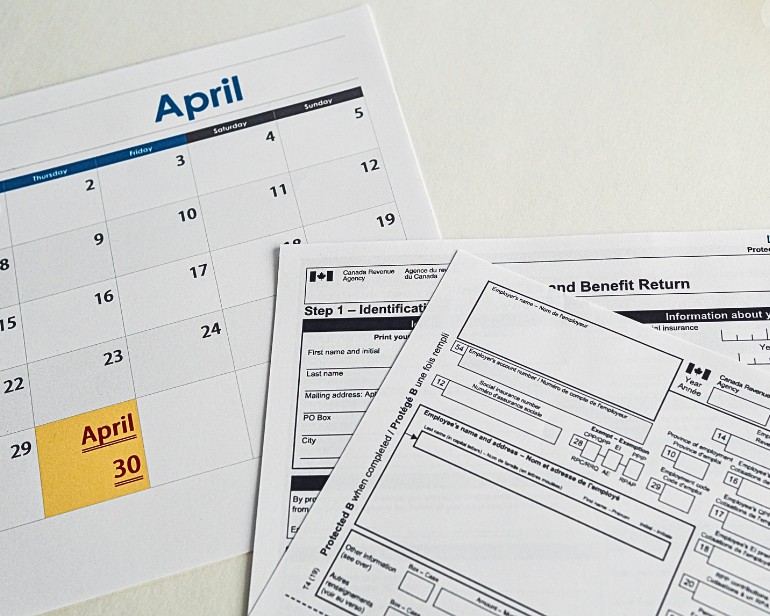

When to file in Canada?

Most years, the deadline for the current year’s income tax in Canada is April 30th of the following year. The only exception I know of for this deadline was during COVID-19 when the government decided to give its citizens a break.

So what does this mean? Also, what happens if you file your taxes late in Canada?

These are very important and common questions. Here in Canada, that deadline is not really for filing your taxes. It is, however, the deadline to pay any outstanding amounts due to the respective government.

There is no actual date by which you must file your taxes in Canada, but if you owe them money, you have until the deadline to pay the bill without penalties and interest.

If you file your returns late, even a few years later, you could be on the hook for interest, which is calculated starting from the due date onwards.

What if you file late but were due a reimbursement?

As stated earlier, there is no issue with filing late. However, if your tax return shows that you should have received a reimbursement, the government will honour it but without interest.

So, for example, if you file a tax return two years late, which showed a reimbursement of $500, you will get the $500 only.

You should be aware that there are other aspects to filing late. If you are entitled to benefits, or if benefits such as Solidarity Tax Credit (for Québec residents) or Canada Child Benefit, which are calculated based on the most recent income tax declaration on file, then these benefits may be suspended or delayed.

This was especially an issue for Québec residents during Covid, where the government of Québec offered relief benefits due to Covid and another to offset inflation.

Both benefits were restricted to citizens who filed their income tax declarations by a specific date. Those who filed after that date lost access to those benefits.

So, what do we include on our taxes?

We start with who we are. We need to tell the person who is processing our tax return who we are by name, where we live, how to communicate with us, and what our I.D. number is.

I have had so many clients ask me why I need to include their date of birth since the government already knows it? The only answer I can give is that it ensures the agents are in the correct client file.

Mistakes happen constantly, so if we provide a SIN(Social Insurance Number) number and date of birth, the agent processing the return can ensure they are processing the correct file.

Next, we include employment information. For some people, this portion is straightforward and possibly the only information to include on their return other than the basics, of course. For others, it is only the starting point.

This section is where we state to the government how much we made at our job, including bonuses, how much your boss removed from your paycheck as source deductions to pay to the government on your behalf and what benefits they paid for on your behalf.

It is not a simple calculation; many people and clients say they do not understand the T4 paper. This situation is not surprising if you are not an accountant or tax preparer.

For most, it looks like a bunch of boxes with numbers that don’t make any sense. To the trained eye, it is a wealth of information.

If you are a Québec resident, you also get the equivalent forms from the Québec government, which has very similar information.

However, there are a few extra pieces to include, such as the Québec provincial income tax deduction, which is separate from the Federal one.

Also, only in Québec, you are required to tell the Québec government how much you made in Tips, and you are taxed on that amount as well.

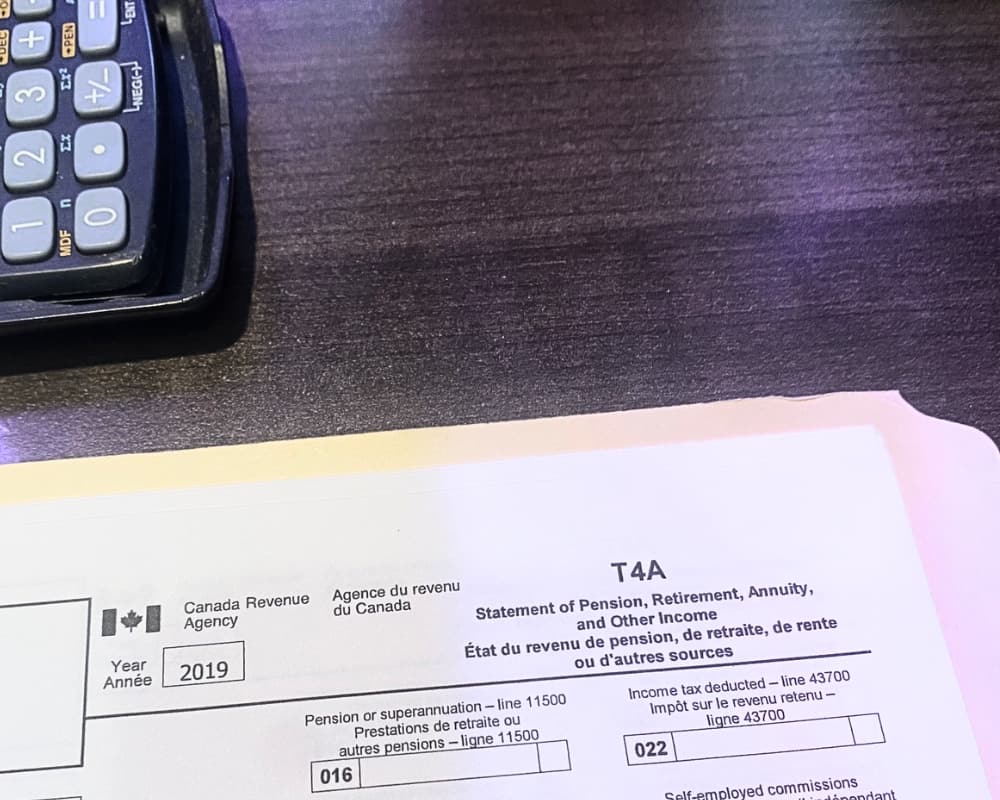

What if you did not work or did not work for a company?

If you did not work, you still need to file a tax return, but it will likely include other income sources such as employment insurance payments, pensions, disability payments, and so on.

These, like the employee tax forms, give a wealth of information that must be declared to the government. Most are taxable with their separate calculations.

If you did not work for a company but did your own thing like Uber, then this becomes a lot more complicated. When you “work for yourself,” you are considered a self-employed individual and, therefore, your own boss.

Consequently, you have to declare to the government as the employee and business information all in one. We discuss this topic in a separate article entitled Business Taxes – How and What to File if self-Employed.

What if you were paid cash?

The rules are the same. You are required to declare ALL income and pay taxes on your total income.

For those paid in cash, the easiest way to declare it is by stating it as self-employment income which as you will read in our Business Taxes – How and What to File if self-Employed article, there are many benefits.

What moneys are not taxable?

You do not have to pay tax on a few types of gains. Some you still need to declare but won’t be taxed on.

An excellent example of this is the proceeds of selling your primary residence. You must report it, but it is only taxed if it is considered a business, either in whole or in part.

This is a relatively new reporting requirement to ensure that people who “flip houses” pay their fair share of taxes.

Some other things that are not taxable include lottery winnings, donations, gifts, inheritances and so on, as they are considered windfalls in the government’s eyes.

Also, reimbursements such as insurance reimbursements are not taxed as they are considered to be reimbursements of after-tax money.

Some incomes are less obvious when it comes to being taxable or not. For example, are disability payments taxable in Canada? That depends on who paid for the insurance.

Generally speaking, if an employer or business owner paid the premium for the disability insurance, then the payout by the insurance company is taxable in the hands of the beneficiary.

But if you pay for disability insurance out of pocket with after-tax money (money that has already been taxed), then the payout is typically non-taxable.

For this, you must verify with the insurance policy and/or your financial security advisor to be sure.

Part of the reason for this is that if a business is paying for the insurance, it usually gets a tax break for that payment, so the benefit becomes a taxable event for the beneficiary(the person who receives the payout).

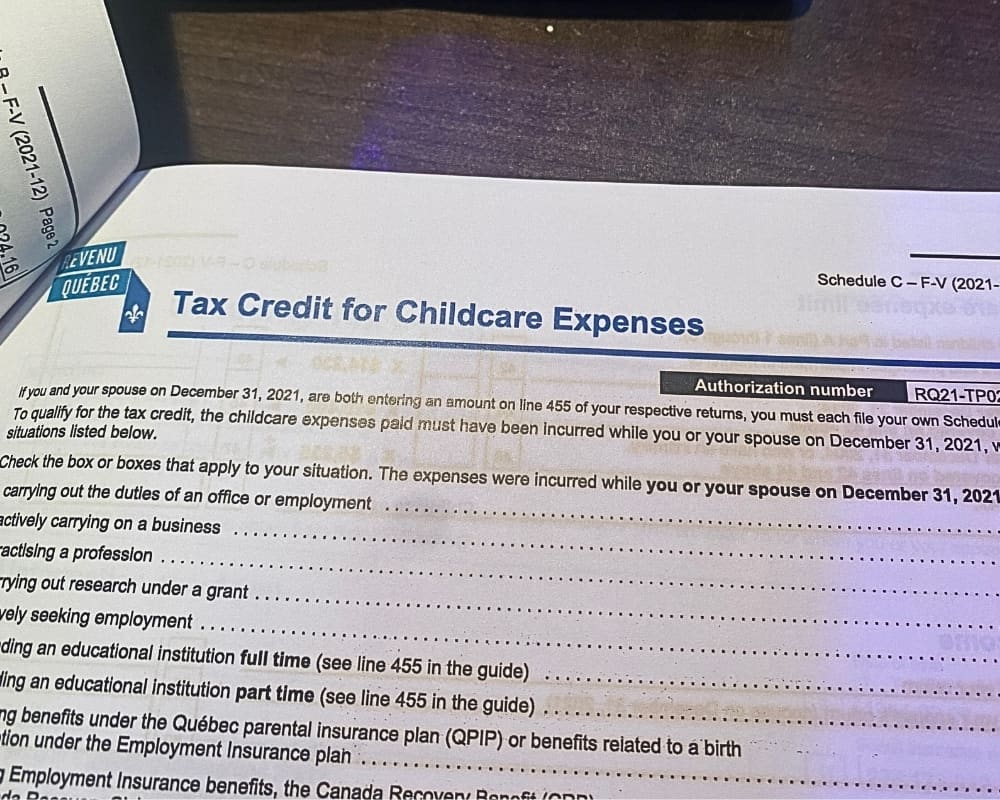

The next part to take into consideration is children.

As parents, we pay a lot of things to raise children. Luckily, the Canadian government does help out a bit. When we claim an underage child on your taxes, it can also allow a benefit such as an eligible dependant credit, the Canadian Child Benefit, and some childcare expenses.

Before July 2016, the Canadian Child Benefit was known as the UCCB (Universal Child Care Benefit), which was a taxable benefit for the parents who received it.

As of July 2016, the benefit was revamped and renamed the CCB (Canadian Child Benefit) and made it non-taxable.

In some provinces, such as Québec, there are a few other benefits to be aware of, such as Québec’s version of the CCB, which also provides parents with a Family Allowance payment.

This supplement is supplied to help with child care expenses, disability care expenses, school supplies, etc.. Québec also offers a benefit for parents looking to adopt a child.

What tax deductions can be used?

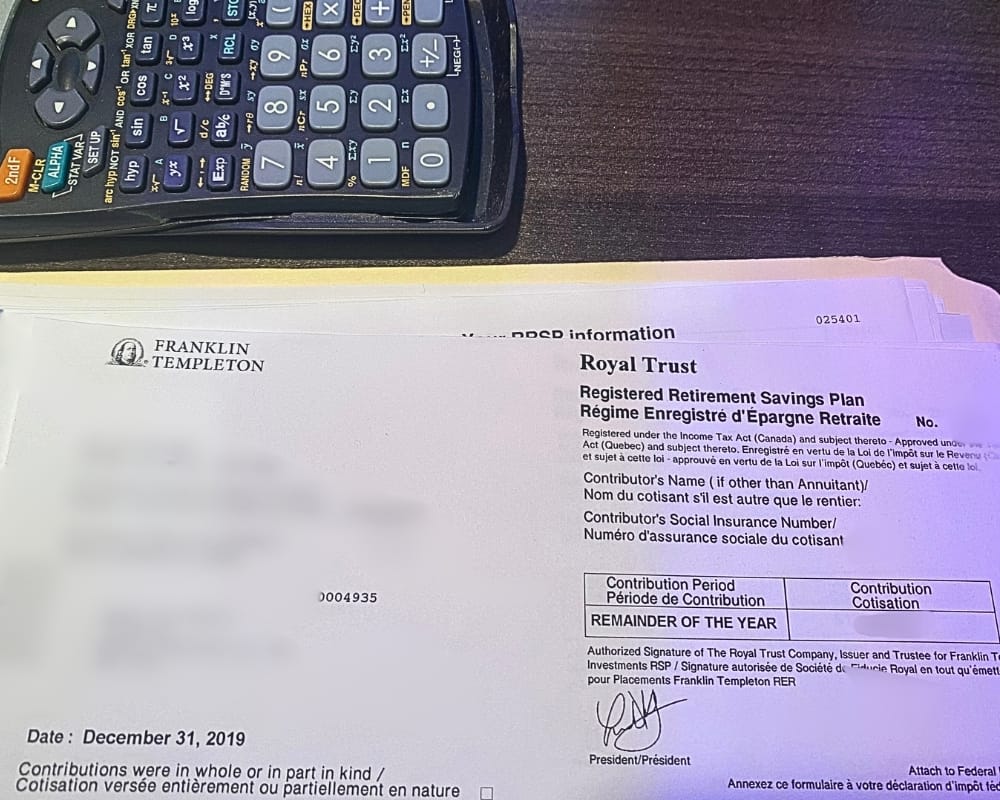

The most commonly used deduction available to Canadians is the RRSP (Registered Retirement Savings Plan). This savings plan was introduced in 1957 was designed to help Canadians save for their retirement.

The basics about how the RRSP helps with taxes is this: if you contribute to an eligible RRSP, the government views that money as pre-tax money(money that has not yet been taxed), so it reduces your Gross income by the amount of the contribution.

To better help explain that, here is a simple example:

Person A: makes $50,000 gross (pre-tax) and makes no RRSP contribution; they get taxed on $50,000.

Person B: makes $50,000 gross (pre-tax) and contributes $10,000; they get taxed on $40,000 instead of $50,000.

Essentially, the contribution amount reduces the gross amount that is taxed in that individual’s marginal tax bracket.

By contributing, you may be able to reduce your taxes by changing the last bracket that you are taxed. We will explain this more after the deductions.

So, what is your RRSP contribution limit?

Lots of Canadians do not understand how their RRSP limit is calculated. It is relatively simple. It is based on your previous year’s income.

Not all incomes qualify for the calculation; however, pensions such as old age security, Canada Pension Plan or the Québec equivalent Québec Pension Plan, dividends, and investment income are not part of the calculation.

So, which incomes qualify? Employment income, Net self-employment income, & Net rental income. The calculation is simple: of the eligible incomes, 18% of the income, up to a maximum, is added to your RRSP contribution limit.

There is a maximum limit amount, which increases each year. The maximum for 2024, since we are heading into the new tax season for the 2023 tax year, is $31,560.

So, if you made $250,000 of eligible income in 2022, your RRSP limit is not increased by $45,000 but rather the maximum of $31,560 for the 2023 tax year.

However, if you made $100,000 of eligible income in 2022, then your RRSP limit will increase by $$18,000.

So what if you do not use that amount? You do not lose it, it is an accumulation limit that increases each year if you have eligible income.

However, if you withdraw some of your RRSP, unlike the TFSA (Tax-Free Savings Account), you do not get the contribution room back.

If you are unsure of what your personal RRSP contribution limit is, there are two places to find out without calling the government.

If you have your Notice of Assessment from the previous year, it is indicated on the second to last page.

Alternatively, you can log into your CRA portal, authenticate yourself and verify both your RRSP limit and TFSA limits under the heading Savings and pension plans.

The next most common deduction to take into consideration is medical expenses. This part is a little more complicated because each province has its own view of which medical expenses are qualifying medical expenses, which are sometimes different for the federal level.

For example, Massage therapist costs are deductible in Ontario, British Columbia, New Brunswick, Newfoundland, and Prince Edward Island but not in Québec, Alberta, Manitoba, Nova Scotia, Saskatchewan, or any of the territories.

For eligible deductions, another restriction is that the amount you can claim must be more than 3% of your Net (after-tax amount) income.

Here, it is helpful to remember that medical expenses are partially transferable within a family unit.

So, suppose you look at a statistically average family, including a husband, wife and two minor kids. In that case, all their medical expenses can be lumped together to make the 3% minimum on one of the parents’ returns.

However, eligible expenses must be for a spouse or, common-law partner or child who is under the age of 18 on December 31st of the current tax year. If the child turns 18 during the year, their eligible expenses cannot be lumped in with the remainder.

What are some of the eligible medical deductions?

Here is a non-exhaustive list of the most common medical deductions:

- Prescription medication,

- Dental care(regular and specialized),

- Eye care,

- Ear care,

- Laboratory tests (including blood tests),

- Prescribed respiratory care (such as CPAP, oxygen, etc.),

- Physiotherapy (not eligible in all provinces),

- Chiropractor (not eligible in all provinces),

These are the most common, but there are many more.

There are some restrictions to be aware of, too. For example, the amount claimed must have been paid out of pocket, cannot have been reimbursed by any insurer (private or group), some may require proof of prescription, and so on.

Here again, getting professional advice is critical, so it is best to verify with your professional tax advisor.

Have you ever wondered the difference between refundable and non-refundable tax credits?

You are not alone; few people understand the difference. Here is a simple way to look at them: if a credit is non-refundable, then the credit can bring down an amount owed to a government to $0, but no further.

If a credit is refundable, then the credit can bring down the amount owed to the government or increase the amount of your tax refund.

To put that in numbers, if you have a tax bill towards the federal government of $100, but you qualify for a $200 non-refundable credit, you will owe them $0. Now, if we use that same example but with a $200 refundable credit, then instead of being $0, you can expect a refund of $100.

So, which are refundable and non-refundable?

Well, that one is more complex. Some tax credits are refundable on a federal level but may or may not be on the provincial level.

For example, charitable donations are non-refundable on the federal level. However, some provinces like Québec allow the credit to be carried forward if not used for up to 5 years.

However, tax credits for medical deductions are generally refundable.

Are you caring for a disabled child/family member?

Many benefits can be claimed on your income tax report for taking care of disabled family members.

For the most part, if you or your child have a disability, you may be eligible for the DTC (Disability Tax Credit), which is an additional tax credit that is unfortunately non-refundable.

To qualify for this credit, you would need to be followed by a doctor who needs to sign off on the disability, and the disability has to be severe and prolonged.

What if you did not know about the DTC?

Luckily, like many federal benefits, if you qualified for the DTC for years that you did not claim it and your following doctor attests to this, you can claim the credit retroactively for up to 10 years.

This credit is also transferable within a family, so a parent can claim it for their child or even a spouse or common-law partner for when they were together.

The purpose of this credit is to offset some of the extra medical expenses for the disability.

Did you know that celiac is part of the DTC?

Are you allergic to Gluten? The federal government has included that ailment in the list of acceptable disabilities that could help you qualify for the DTC.

Also, to qualify, you can have multiple issues that, when combined, can satisfy the requirement for the Disability Tax Credit.

If you feel you may be eligible, download the form T2201 from canada.ca and speak to your doctor. Small side note: Québec also has a version of the DTC, which you surprisingly don’t need a separate form filled out for it; if Canada qualifies you, Québec will likely do too.

Other deductions?

There may be other deductions that may apply to you, and some that come and go.

An example of this is moving costs. In some specific cases, moving expenses can be claimed on your income tax.

The most common is if you moved more than 40kms for work or school. Generally, temporary work does not allow this, but a permanent move can.

Here again, it is best to speak with your professional tax advisor to see what deductions have been implemented for that tax year and at what level (province or Canada-wide).

To better explain this, for years before July 2017, Canada allowed the deduction of public transportation on income taxes but stopped that incentive as of July 2017.

However, Ontario continued with its tax credit for Ontario seniors for eligible public transit with a limit of $3000.

Home renovations are also a common question about deductions, and here again, the answer is both yes and no. Or rather, it depends.

In some years, some government agencies have encouraged particular renovations, such as changing the insulation, changing the windows and doors, upgrading heating systems, etc.

Sometimes, these expenses can be claimed on your income taxes; sometimes, provincial grants are paid out upon approval of eligible upgrades.

But one statement is always true: the benefit will never pay for the upgrade but will help offset some of the costs.

However, there is another way that specific home renovations can be claimed as of the 2023 income tax year.

This credit is intended for qualifying families to create a self-contained secondary unit for Multigenerational homes.

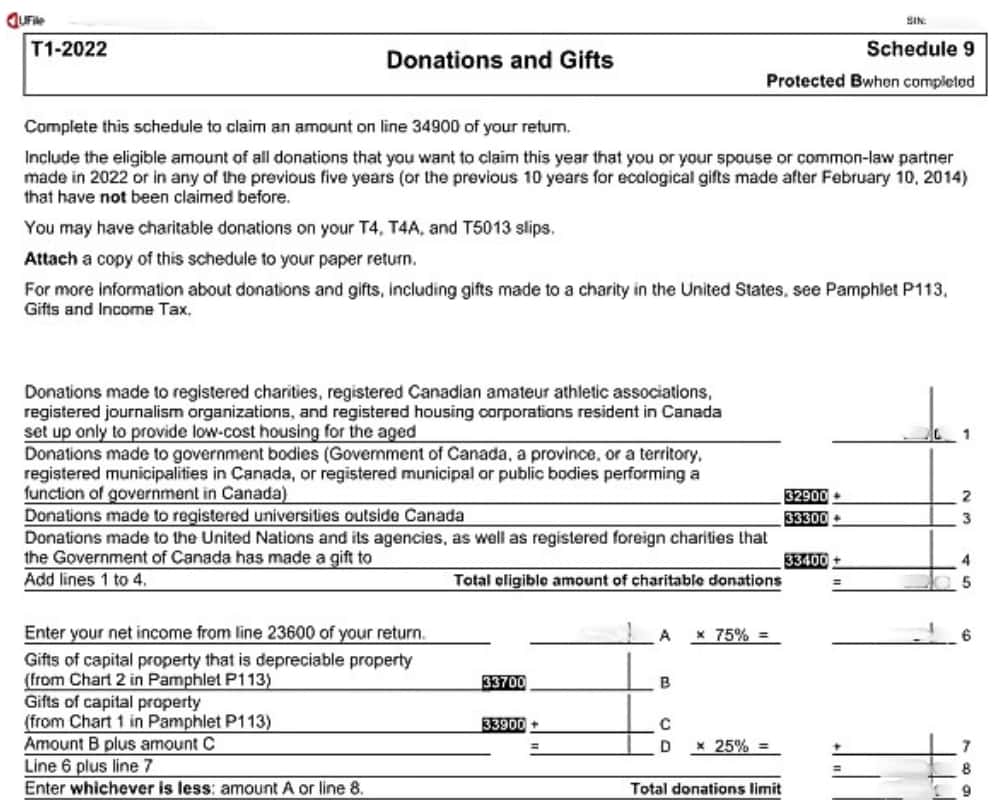

What about charitable donations? Are they deductible?

The final deduction that we will discuss here is donations. Yes, some donations are tax deductible.

The most common are cash donations (typically of an amount higher than $25) to a registered institution. This is a fancy way of saying a business (profitable or non-profit) that is registered with the government to accept donations in exchange for a tax receipt.

The most common are religious institutions, educational institutions, political parties, etc. So you give them money, get a receipt for said money, and you claim it.

However, keep in mind that it is NOT a dollar-to-dollar deduction. As a general rule of thumb, if the donation is for $200 or less, the tax credit is usually 15%.

If you donate $200 to the Red Cross, for example, you would get a $30 tax credit.

What is the Marginal Tax Bracket or Marginal Tax Rate?

As mentioned earlier, now that we’ve covered the common deductions, let’s discuss the Marginal Tax Bracket. So what is it?

In Canada, we use a progressive tax system. This calculation starts at $0 and works upwards in portions (aka income tax brackets). However, we are entitled to a basic personal amount.

Here, we will show the current federal 2023 tax year rate in a table. These are the federal numbers only, as each province and territory has its provincial tax rates and income thresholds over and above the federal level:

| Tax Rate | Taxable Federal income tax rates threshold | ||

| 15% | Income of $55,867 or less | ||

| 20.5% | Income between $55,867.01 up to $111,733. | ||

| 26% | Income between $111,733.01 to $173,205. | ||

| 29% | Income between $173,205.01 to $246,752. | ||

| 33% | Income of $246,752.01 and more. | ||

So what does that mean? In short, your Federal Marginal Tax Bracket is the level at which your last dollar is calculated.

So, if you made $50,000, your federal marginal tax bracket is 15%. If you made $100,000, then your federal marginal tax bracket is 20.5%.

However, you do not pay 20.5% on all of the $100,000, only on the amount between $55,867.01 and $100,000.

Here, I need to point out two essential items.

First, YOUR marginal tax bracket is the percentage of tax rate of BOTH federal and provincial levels combined.

So, if you are in B.C. using the same two examples as before, at $50,000, your marginal tax bracket is 22.7% (15% for federal plus 7.7% for B.C.).

For an income of $100,000, your marginal tax bracket is 31% (20.5% federal plus 10.5% for B.C.).

The second essential item for Québec is that since we have to be different, there is another calculation to take into consideration, which is the tax abatement.

This is a percentage that is removed from the federal tax amount total, currently 16.5%, in exchange for the fact that Québec takes care of its own financial system, AKA Revenu Québec.

Where to live in Canada, tax-wise?

In Canada, where you reside, December 31st of the current year is the deciding factor of who you pay your provincial taxes to.

So, if you live in Saskatchewan on December 31st of 2023, then you pay Canada and the province of Saskatchewan based on their calculations.

From a strictly tax viewpoint, where in Canada do you keep the most of your income?

Since all Canadians have the same Federal tax rate, except for Québec, we need to look at each province’s tax rates.

To keep this short and sweet, we’ll give you the answer. The place in Canada to live with the lowest tax rate on the low end is Nunavut, where the minimum provincial income tax rate is 4%.

On the high end, for those making $246,752.01 or more, the worst place to reside is in Québec, with a whopping 25.75%.

To make this make more sense, if you earn $300,000 while living in Québec, your marginal tax bracket is 58.75%(minus the federal tax abatement), so for every dollar you earn over $246,752.01, you are giving the government over $0.50 of that dollar (not taking into account the federal abatement).

What receipts should you keep?

The simple answer for most people is all tax slips you received, as well as any receipt you used for deductions like medical expenses.

According to the CRA, these documents should be kept for at least six years following the tax year. However, as a professional tax advisor, I always recommend to keep them for ten years.

It sounds like a lot of paper that will take up a lot of precious room. However, there is a solution, here are the recommendations.

Recommendations.

Start with the records, which, as stated above, keep them for ten years. However, in our digital age and for safety reasons, do not keep paper.

I always suggest that my clients digitize all relevant documents and keep digital copies. Ten years’ worth of income taxes, including all receipts, can fit on a thumb drive in the palm of your hand.

Some issues with paper copies are things like fire, water, and improper filing, and the worst issue is that with regular receipts along with some forms, the information disappears over time.

Trying to prove that you paid hundreds of dollars on medical equipment seven years ago with a blank receipt will make you feel like a fool.

So, digitize the receipt. Scan it and name it appropriately so you can find it.

Doing it like this has an added benefit: if you need to find a receipt for X in 2018, finding a digital copy is much easier than pulling out a 3/4″ file folder, leafing through each sheet and finding a blank receipt.

Additionally, make a copy or use a personal cloud service that allows you to back up your documents.

As a professional tax advisor, I use a secure cloud server with end-to-end encryption for security and privacy reasons. It is also a great way to share sensitive documents securely.

What’s left?

To wrap this up, here are a few reminders to keep in mind.

All residents in Canada, excluding some minors, are required to file their taxes each year if they made an income or not.

Minors must file if they made an income but typically get the majority back. The deadline to pay an outstanding balance is usually April 30th of the year following the taxation year.

The best way to know if you have a balance owing or not is to sign into your own CRA portal, either with an access code or through their partner sign-in, which is through your personal bank using your online banking credentials.

Once again, for more details about Uber, sole proprietorship, or other self-employment, please see our article Business Taxes – How and What to File if self-Employed, where we will break it down for you.

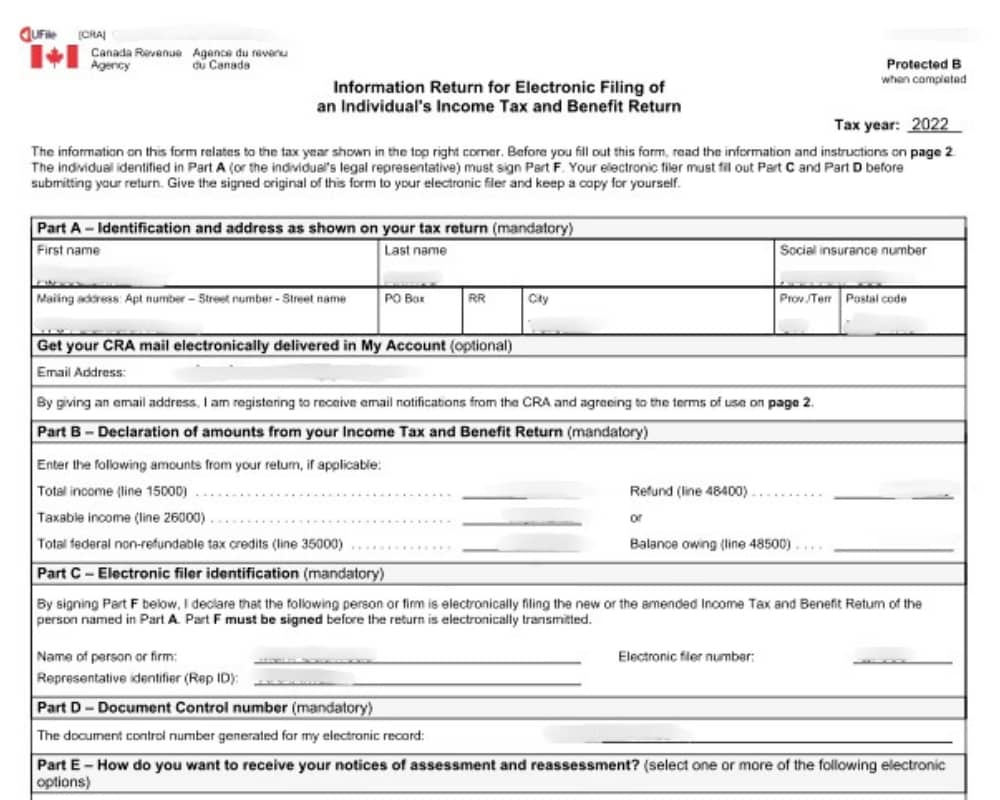

Finally, the best way to send in your tax returns is electronically. Like us, the government does not really want to be overloaded with papers.

Not to mention, they are not responsible if a piece of the return disappears.

Can you imagine 75% of Canada’s population were to send in a paper return with all the relevant receipts? That would be over 29 Million envelopes, each with at least 10 pages.

So, the government prefers we send them an electronic copy that they can view on a computer screen and have far fewer errors or misunderstandings.

This is another reason why I highly suggest using tax software. Not all are equal, but most will get the job done.

One last word: if you are having trouble paying your taxes due, whether to the federal government or provincial, don’t ignore the problem; communicate with them.

They are there to help and can work with you to find a solution.

Also, if you are looking for a professional tax advisor to help you, we can help you there. If you have general questions, feel free to reach out to us or contact one of our specialists at www.gauvreauetfamille.ca.